As a business owner, it’s essential to plan ahead and determine how your business should progress in your absence. Business estate planning helps you protect your interests and prepare affairs for the next generation. It can also allow you to reduce taxes on your estate and mitigate potential disputes.

There are several things to consider when creating your business estate plan. For example, the type of business you operate and the assets you own can help you strategize your succession plan. Your succession plan can also determine the best tool to distribute and manage your estate during your lifetime or after death.

What Is Estate Planning for Business Owners?

Business estate planning involves deciding and arranging how business assets should be distributed or utilized after the owner’s death or in the event of the owner’s incapacity. You can dictate how your company should be managed and who should inherit the proceeds. It also helps you handle potential risks, taxes and disputes. In other words, it involves creating a succession plan for when the business owner is no longer able to manage the business’ affairs.

Entrepreneurs devote time, effort and money to building businesses— sometimes from scratch — and cannot imagine their investments going to waste. When properly managed, a company can survive decades, creating a legacy for future generations. One of the most effective ways to ensure long-term success for your business is developing a good estate plan.

Leaving your business unplanned can result in many challenges. For example, if a business owner dies intestate, or without a valid will, state law can dictate how their assets are distributed — including their business assets. Sometimes, this may contradict the owner’s wishes.

The persons who inherit the business may have different visions or insights, potentially affecting business continuity. Forward-thinking business owners usually consider all these factors and take proactive steps to ensure a smooth transition.

You can use several tools to plan your business estate, including wills and trusts, powers of attorney and buy-sell agreements.

Estate Planning Considerations for Business Owners

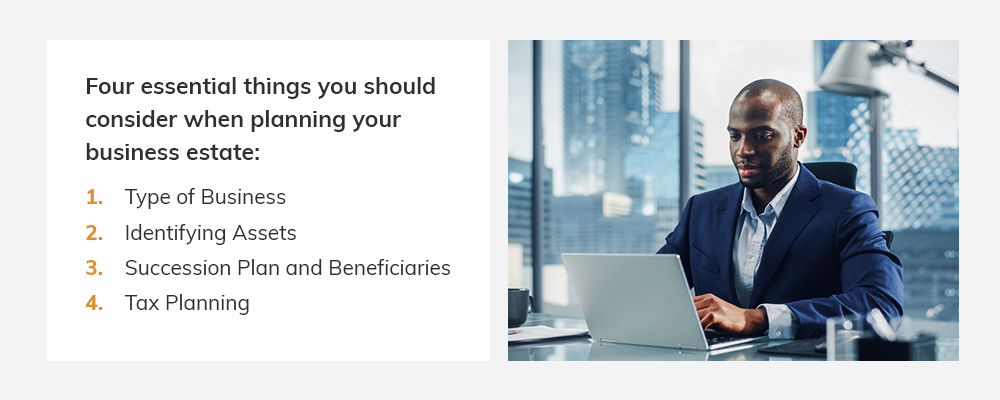

There are four essential things you should consider when planning your business estate. These are:

1. Type of Business

There are different types of businesses, including sole proprietorship, limited partnership, limited liability partnership, general partnership, limited liability company and corporation. Each type can affect how you manage your assets and liabilities.

For example, if you operate a sole proprietorship, you will likely own all or most company assets. Business owners who run other kinds of businesses, like limited liability companies (LLCs) or general partnerships, may share the assets with other business members or owners.

Asset identification and distribution can be complex depending on the nature of the business, so it’s essential to contact a trusted professional when making decisions.

2. Identifying Assets

Assets can be tangible or intangible. Examples of tangible business assets are real estate, vehicles, equipment and inventory. Intangible assets include intellectual property and goodwill.

Business owners should take inventory of all their assets and determine who they wish to inherit them.

3. Succession Plan and Beneficiaries

Business succession planning involves strategizing how you wish your business to progress after death. It considers issues like inheritance and management, preparing your affairs for the next generation. Your beneficiaries may be your spouse, children, a charity or any other person capable of holding property. Identifying your assets and potential beneficiaries helps you create a good succession plan.

We can categorize succession plans into internal and external to make things simple.

Internal Succession

Internal succession is where you transfer business ownership, and potentially leadership, to one or more key employees. Typically, business owners use this approach when they wish to keep the business within their trusted circle.

The owner of a family business, for example, might pass the business to their spouse, children or siblings. You can also plan each successor’s level of involvement in running the company, like mentoring and gradual ownership transfer. Without a suitable family successor, the owner may sell the business to some employees through a management buyout. The advantage of internal succession is that your business can continue growing with people already familiar with its operations.

These are a few examples. The option you select depends on the peculiarities of your case, so it’s best to consult a professional for guidance.

External Succession

External succession involves selling your business to third parties, such as strategic buyers, private equity firms or competitors. The option may be practical when the buyer is more suitable than your internal successors.

Selling your business to competitors or strategic buyers can be challenging. It allows them to gain your market share and customer base. On the other hand, such arrangements can be beneficial if you sell it for a reasonable price. The key is to negotiate favorable terms to protect your interests.

Some business owners prefer selling their businesses to private equity investors. The option can drive growth while the original owner retains partial ownership. A complete sale is also possible. Private equity firms can bring expertise and resources to the business.

Business owners can combine the benefits of internal and external succession plans. For example, an employee stock ownership plan (ESOP) allows employees to own a piece or all of the company they work for. Alternatively, the business owner can partner with a strategic investor to invest resources into the business for a portion of the proceeds.

4. Tax Planning

A proper business estate plan can reduce the tax burdens on your estate. For example, establishing a trust, gifting the property or utilizing valuation discounts can help you minimize estate, capital gains or income taxes on the estate.

Contrary to federal taxes, state tax law may vary from state to state, so it’s essential to speak with an estate planning attorney for personalized advice.

Business Estate Planning Tools

Here are five tools you can use to plan your business estate:

- Wills: A will is a document that details how a person’s estate should be distributed after their death.

- Trusts: A trust is an arrangement that allows another person to hold your properties on behalf of the beneficiaries. While a will takes effect after your death, a trust can take effect during your lifetime.

- Powers of attorney: This legal document gives another person authority to act on your behalf during your lifetime. The person’s financial or legal actions can bind the business owner. Most often, a power of attorney can be helpful in allowing a business to continue operating even when the owner is experiencing health complications or incapacity.

- Buy-sell agreements: These are legally binding agreements that detail the terms of a business interest transfer when the business owner dies or suffers from an incapacity. The contract usually states who should take over the business and at what price. It can also specify how the assets should be managed.

- Life insurance: This can provide liquidity to your estate and ensure your business transfers smoothly to the new owner. A financial advisor or experienced attorney can help you determine the appropriate life insurance coverage for your business estate plan.

Learn More About Business and Estate Planning

Consulting an attorney can help you avoid some estate planning mistakes. Even so, you should partner with a lawyer who understands your needs. Barulich Dugoni & Suttmann Law Group is an estate planning law firm with over 30 years of experience. We are dedicated to creating value for clients by helping them strategize ways to manage and distribute their assets for long-term success.

If you have any questions about business and estate planning or want to know how we can help you, contact us now!